Source:

Dr Shane Oliver

Head of Investment Strategy and Economics and Chief Economist, AMP Capital

Key points

- 2018 saw reasonable global economic and profit growth and still low interest rates but it has been a rough year for investors with worries about the Fed, trade wars and global growth causing volatility and poor returns.c

- 2019 is unlikely to see the plunge into recession many fear with growth likely to stabilise supporting profit growth, the Fed is likely to undertake a pause in rate hikes and global monetary policy is likely to remain easy. The RBA is expected to cut interest rates.

- Against this backdrop, share market volatility will likely remain high but markets should start to improve through the year.

- The main things to keep an eye on are: the risks around the Fed, US/China tensions, global growth, Chinese growth and the property price downturn in Australia.

2018 – a lot weaker than expected

After the relatively low volatility and solid returns of 2017, the past year has seen almost the complete opposite with high volatility and poor returns. It started strongly in January but started to get messy from February. At a big picture level things were fine: global growth looks to have held solid at around 3.7%, inflation rose in the US but only to target and it remained low elsewhere, the Fed raised interest rates but rates generally remain low and profits rose solidly. But it was the risks below the surface that came together to give a rough ride. There were five big negatives:

- Fear of the Fed. The Fed provided no real surprises and nor did US inflation, but investors became increasingly nervous that Fed hikes would crush US growth and profits.

- US dollar strength. While the US dollar did not rise above its 2016 high it caused problems in the emerging world where US dollar denominated debt is high.

- President Trump’s trade war. This was always a high risk for 2018 and once it got underway it weighed on share markets. While the initial focus seemed to be the US versus everyone it morphed into fears of a new Cold War with China adding to fears about growth and profits.

- China slowdown. This was as expected to around 6.5% as a result of credit tightening but fears that it will combine with the trade war and get worse added to global growth angst.

- Global desynchronisation. US growth was strong, but it slowed in Europe, Japan, China and the emerging world.

Australia saw growth around trend and made it through 27 years without a recession, as infrastructure spending, improving business investment and strong exports helped support growth and this in turn drove strong employment growth, a fall in unemployment and the Federal budget closer to a surplus. Against this though credit conditions tightened significantly with the Royal Commission adding to regulatory pressure on the banks, house prices fell, wages growth edged up but remained weak and inflation remained below target, all of which saw the RBA leave rates on hold.

Overall this drove a volatile and messy investment environment.

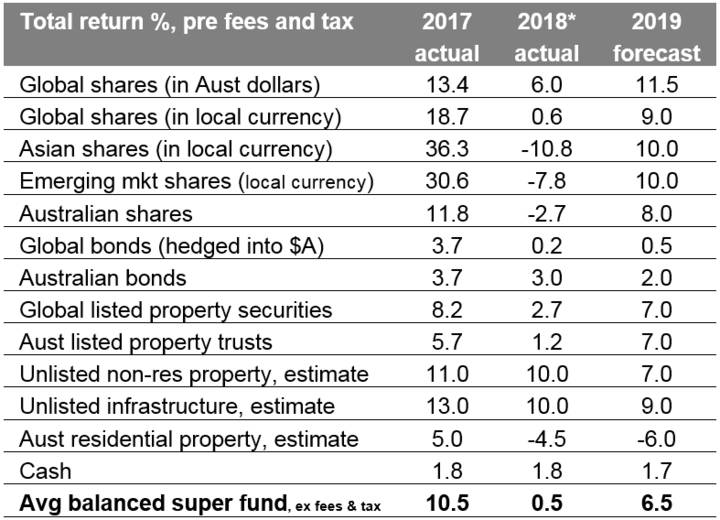

Investment returns for major asset classes

- Global shares saw weak returns in local currency terms with significant corrections around February and October. But this masked positive returns from US shares but weakness elsewhere. Global share returns were boosted on and unhedged basis because the $A fell.

- Asian and emerging market shares paid the price for being star performers in 2017 with losses thanks to a rising $US causing debt servicing fears, the US trade war posing a threat to growth and political problems in some countries.

- Australian shares were hit by worries about the banks, consumer spending in the face of falling house prices and weakness in yield-sensitive telcos and utilities offsetting okay profit growth and low interest rates.

- Government bonds yet again had mediocre returns reflecting low yields and capital losses from rising yields in the US as the Fed hiked. Australian bonds outperformed.

- Real estate investment trusts remained constrained on the back of Fed tightening and higher bond yields.

- Unlisted commercial property and infrastructure continued to do well as investors sought their still relatively high yields.

- Commodity prices were weak on global growth worries and the oil price had a roller coaster ride, first surging ahead of US sanctions on Iran then crashing as demand fell.

- Australian house prices fell led by Sydney and Melbourne.

- Cash and bank term deposit returns were poor reflecting record low RBA interest rates.

- Reflecting US dollar strength, the $A fell not helped by a falling interest rate differential and lower commodity prices.

- Reflecting soft returns from most assets, balanced superannuation fund returns were soft.

2019 – better, but volatility to remain high

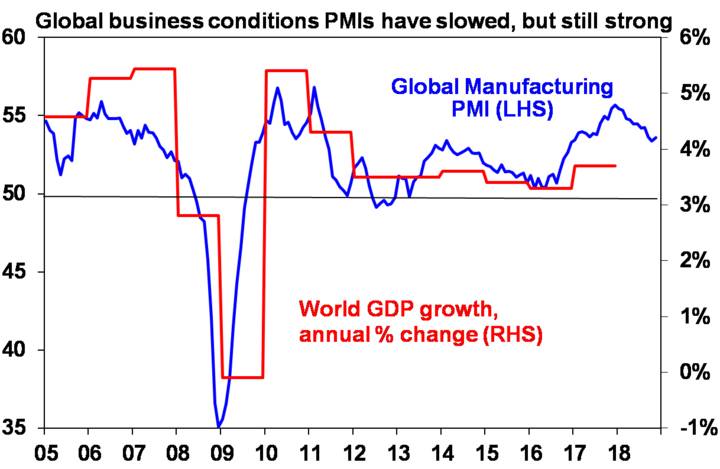

In a big picture sense, the global economy looks to be going through a mini slowdown like we saw around 2011-12 and 2015-16. This is most evident in business conditions indicators that have slowed but remain okay. See the next chart.

Like then, this has not been good for listed risk assets like shares but it’s unlikely to be signalling the start of a recession, baring a major external shock. Monetary conditions have tightened globally but they are far from tight unlike prior to the GFC and the normal excesses in the form of high inflation, rapid growth in debt or excessive investment that precede recessions in the US or globally are absent. In fact, to the extent that the softening in growth now underway takes pressure off inflation and results in easier monetary conditions than would otherwise have been the case it’s likely to extend the cycle, ie delay the next recession. The slump in oil prices is a key example of this in that it will take some pressure off inflation and provide a boost to consumer spending. Against this background the key global themes for the year ahead are likely to be:

- Global growth to stabilise and then resynchronise. Global growth is likely to average around 3.5% which is down from 2018 but this is likely to mask slower growth in the first half of the year ahead of some improvement in the second half as China provides a bit more policy stimulus, the Fed pauses in raising interest rates, the fall in currencies against the $US dollar provides a boost to growth outside the US and trade war fears settle down (hopefully). Overall, this should support reasonable global profit growth.

- Global inflation to remain low. With growth dipping back to around or just below trend in the short term and commodity prices down inflation is likely to remain low. The US remains most at risk of higher inflation due to its tight labour market, but various business surveys suggest that US inflation may have peaked for now at around 2%.

- Monetary policy to remain relatively easy. The Fed is likely to have a pause on rate hikes during the first half and maybe hike only twice in 2019 as it gets into the zone that it regards a neutral. Rate hikes from other central banks are a long way away. In fact, further monetary easing is likely in China and the European Central Bank may provide more cheap funding to its banks.

- Geopolitical risk will remain high causing bouts of volatility. The main focus is likely to remain on the US/China relationship and trade will likely be the big one. While Trump is likely to want to find a solution on the trade front before tariffs impact the US economy significantly & threaten his re-election in 2020, it’s not clear that this will occur before the March 1 deadline from the Trump/Xi meeting in Buenos Aires so expect more volatility on this issue. Wider issues including the South China Sea could also flare up along with negotiations around Italy’s budget.

In Australia, strength in infrastructure spending, business investment and export values will help keep the economy growing but it’s likely to be constrained to around 2.5-3% by the housing downturn and a negative wealth effect on consumer spending from falling house prices. This in turn will keep wages growth slow and inflation below target for longer. Against this backdrop the RBA is expected to cut the official cash rate to 1% with two cuts in the second half of 2019.

Implications for investors

With uncertainty likely to remain high around US interest rates, trade and growth, volatility is likely to remain high in 2019 but ultimately reasonable global growth & still easy global monetary policy should drive stronger overall returns than in 2018:

- Global shares could still make new lows early in 2019 (much as occurred in 2016) and volatility is likely to remain high but valuations are now improved and reasonable growth and profits should see a recovery through 2019.

- Emerging markets are likely to outperform if the $US is more constrained as we expect.

- Australian shares are likely to do okay but with returns constrained to around 8% with moderate earnings growth. Expect the ASX 200 to reach around 6000 by end 2019.

- Low yields are likely to see low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but it’s slowing.

- National capital city house prices are expected to fall another 5% led again by 10% or so price falls in Sydney and Melbourne as tighter credit, rising supply, reduced foreign demand and potential tax changes under a Labor Government impact.

- Cash and bank deposits are likely to provide poor returns.

- The $A is likely to see more downside into the high $US0.60s, as the gap between the RBA’s cash rate and the Fed Funds rate goes further into negative.

What to watch?

After the turmoil of 2018, the outlook for 2019 comes with greater than normal uncertainty. The main things to keep an eye on in 2019 are as follows:

- US inflation and the Fed – our base case is that US inflation stabilises around 2% enabling the Fed to pause/go slower, but if it accelerates then it will mean more aggressive tightening, a sharp rebound in bond yields and a much stronger $US which would be bad for emerging markets.

- The US trade war – while it may now be on hold thanks to negotiations with China, Europe and Japan these could go wrong and see it flare up again. US/China tensions generally pose a significant risk for markets.

- Global growth indicators – if we are right growth indicators like the PMI shown in the chart above need to stabilise in the next six months.

- Chinese growth – a continued slowing in China would be a major concern for global growth and commodity prices.

- The property price downturn in Australia – how deep it gets and whether non-mining investment, infrastructure spending and export earnings are able to offset the drag from housing construction and consumer spending.